What “Newstown CraigScott Capital” Actually Means in Public Records

When people search newstown craigscottcapital or newstown craig scott capital, they usually expect a modern investment firm. What they often find instead is a mix of archived references, regulatory entries, and republished summaries that don’t always align cleanly.

This is where confusion starts. The name Newstown CraigScott Capital / Craig Scott Capital, LLC appears in older brokerage-related contexts tied to the United States financial system. It is not always clear whether a search result reflects an active firm or a historical reference pulled from archived FINRA BrokerCheck data or secondary reporting.

The key idea here is simple: search engine visibility does not equal active legitimacy. Many investors misread online presence as confirmation of current operations, which can lead to misunderstanding.

Craig Scott Capital – Verified Historical Profile

Legal entity overview and formation details

Craig Scott Capital, LLC is associated with a U.S.-registered broker-dealer structure that operated under regulatory oversight. Its identity appears in historical filings tied to Uniondale, New York, United States, and is often referenced through its CRD #155924 (Central Registration Depository number).

This CRD number is critical because it connects the firm’s identity across regulatory systems. Without it, investors often mix up similar names or outdated references.

The important takeaway is that legal identity always matters more than branding. A firm name can appear active online while the underlying registration status tells a different story.

Business model and services

Like many legacy retail brokerage firms, Craig Scott Capital operated in a structure where brokers executed trades and provided wealth management or financial advisory services.

Revenue typically came from:

- Trading commissions

- Sales-driven compensation models

- Product-based incentives

This model created a direct link between trading activity and revenue generation. In simple terms, more trading often meant more earnings for the firm.

That structure is one reason regulators pay close attention to firms like this.

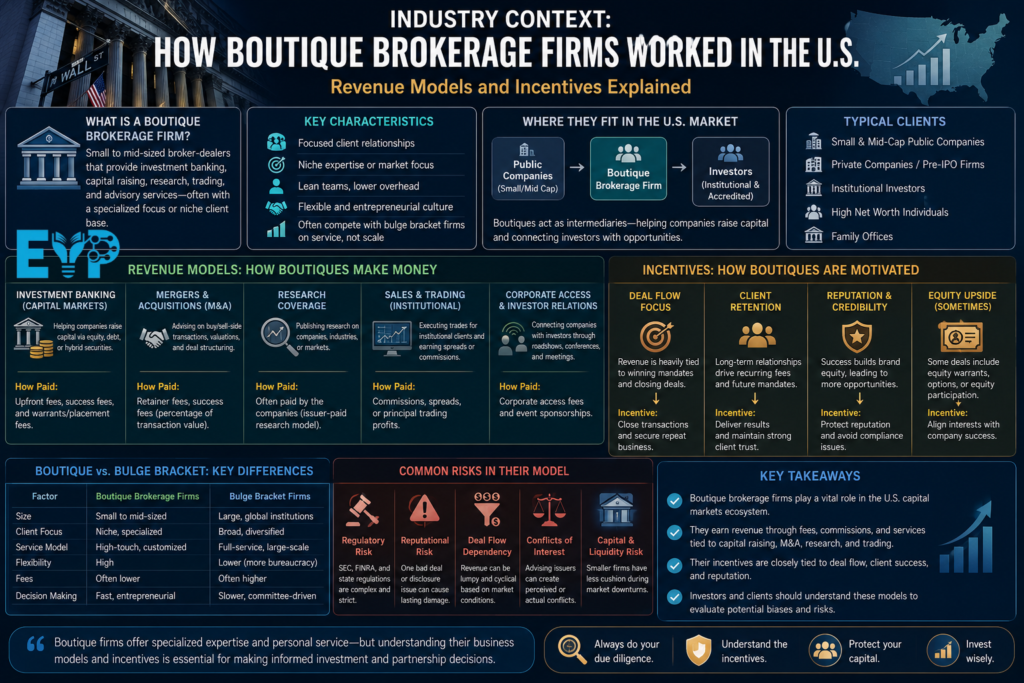

Why boutique brokerages existed

Boutique firms filled a gap between large institutions like Fidelity Investments, Charles Schwab, and Vanguard, and smaller retail investors who wanted personalized attention.

They offered:

- Access to market trading

- Personalized broker relationships

- Entry into structured investment products

But they also carried structural risks tied to incentives and oversight.

Industry Context: How Boutique Brokerage Firms Worked in the U.S.

Revenue models and incentives

Most boutique brokerages operated on a commission-based revenue model. Brokers earned money when clients traded, not necessarily when clients profited.

This created what experts call a transaction-based revenue conflict. The more trades executed, the higher the revenue, regardless of long-term performance.

Over time, this structure became controversial because it often encouraged higher trading frequency, sometimes beyond what investors actually needed.

Sales culture and structural pressure

Many firms in this category developed aggressive sales environments. Brokers were incentivized to generate activity, which sometimes led to practices like churning (excessive trading).

Even when not intentional, this model blurred the line between advice and sales.

Modern comparison

Today, firms like Betterment, Vanguard, and Fidelity Investments lean toward:

- Passive investing

- Lower-cost structures

- Long-term portfolio allocation

That shift reduced many of the conflicts seen in older brokerage models.

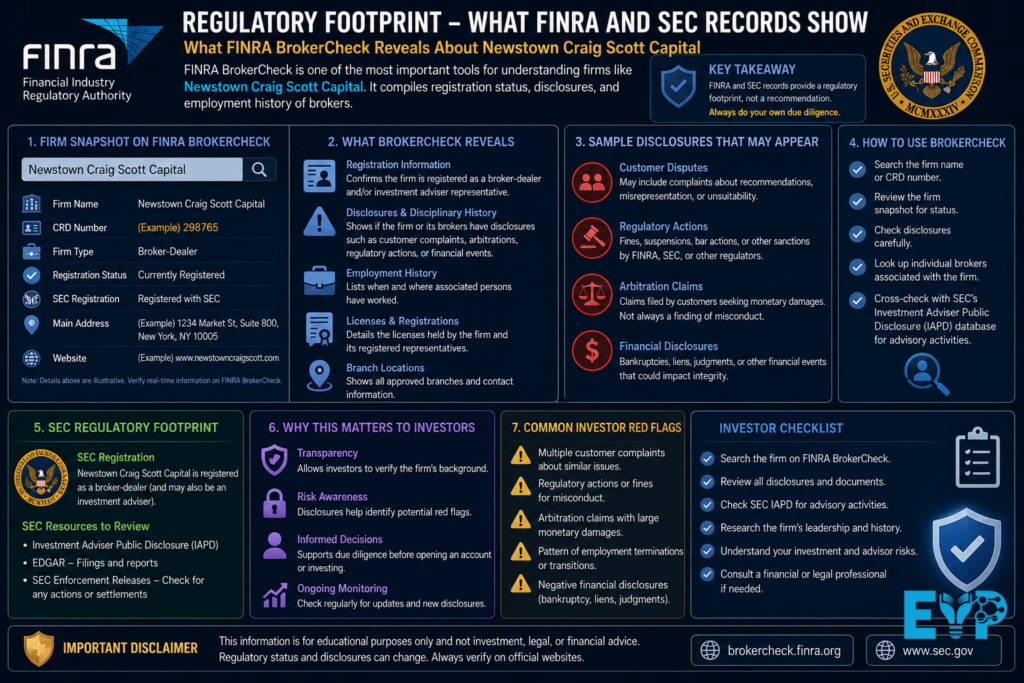

Regulatory Footprint :What FINRA and SEC Records Show

What FINRA BrokerCheck reveals

FINRA BrokerCheck is one of the most important tools for understanding firms like Newstown Craig Scott Capital. It compiles registration status, disclosures, and employment history of brokers.

For investors, this tool answers three key questions:

- Is the firm registered?

- Who worked there?

- Were there any disciplinary actions?

This is where transparency becomes measurable instead of theoretical.

SEC registration and public disclosures

The SEC Investment Adviser Public Disclosure system provides another layer of visibility, especially for advisory services. Firms may appear in Form ADV filings, which outline business structure, fees, and conflicts of interest.

If a firm does not appear cleanly in SEC records, that gap itself becomes a signal worth paying attention to.

Interpreting regulatory data correctly

Not all disclosures mean wrongdoing. However, patterns matter.

Repeated issues such as:

- Disciplinary action

- Enforcement action

- Disclosure history flags

can indicate systemic risk rather than isolated incidents.

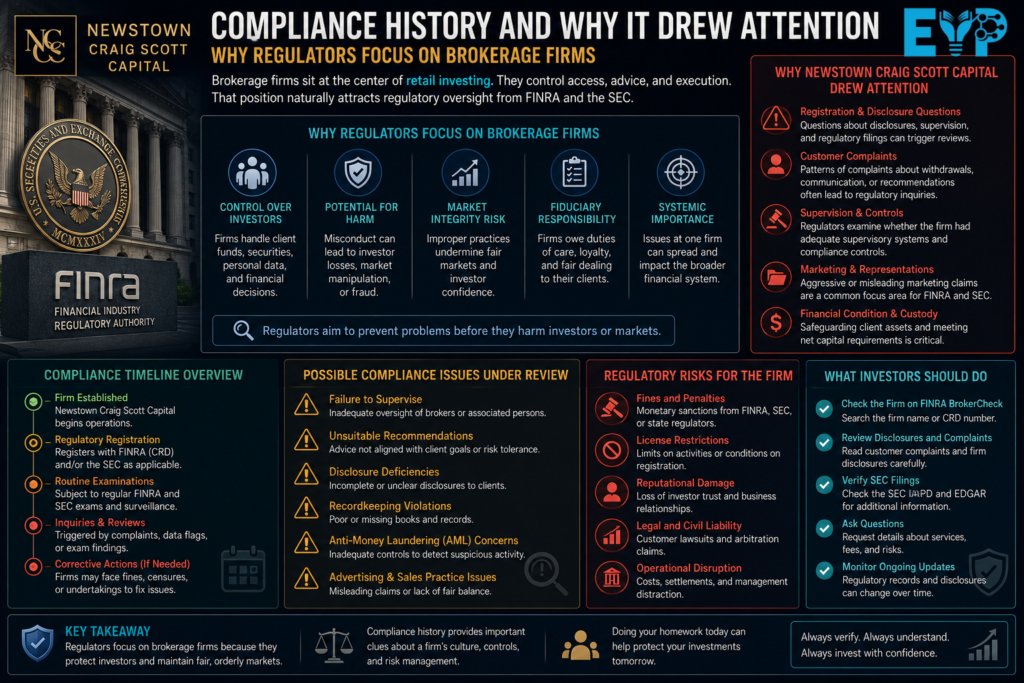

Compliance History and Why It Drew Attention

Why regulators focus on brokerage firms

Brokerage firms sit at the center of retail investing. They control access, advice, and execution. That position naturally attracts regulatory oversight from FINRA and the SEC.

Regulators look for patterns that might harm retail investors, especially in environments where sales incentives are strong.

Common industry issues

Across similar firms, regulators often examine:

- Unsuitable investment recommendations

- Excessive trading patterns

- Misleading product explanations

These are not unique to one company but are common risk areas in the industry.

What enforcement actually means

An enforcement action does not always mean fraud. Sometimes it reflects compliance failures or procedural violations.

However, repeated actions can suggest deeper structural problems in how a firm operates.

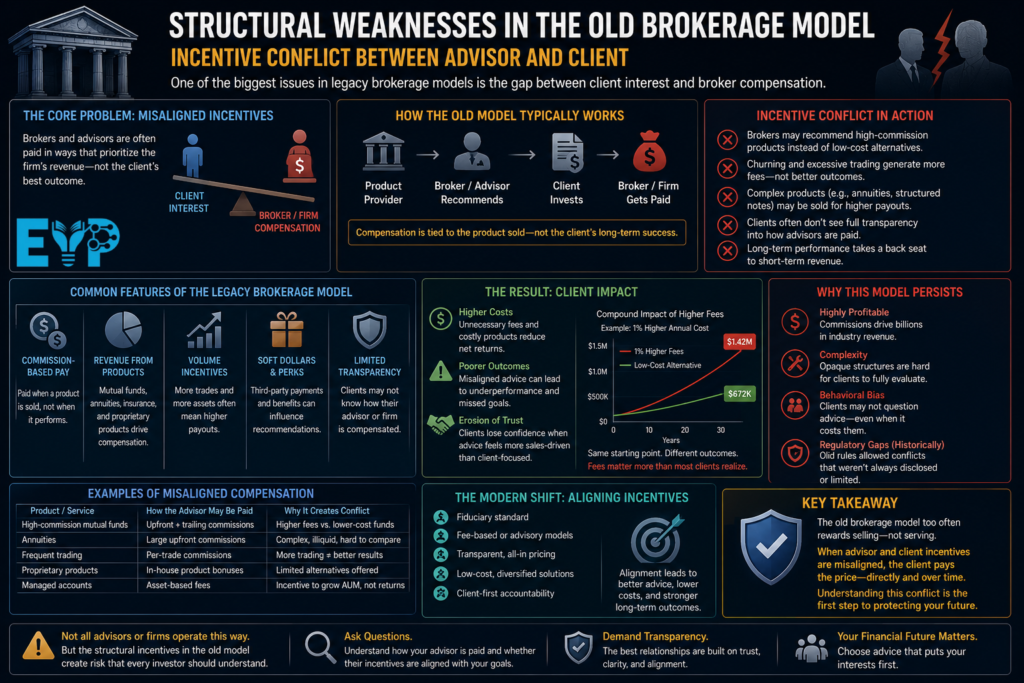

Structural Weaknesses in the Old Brokerage Model

Incentive conflict between advisor and client

One of the biggest issues in legacy brokerage models is the gap between client interest and broker compensation.

When revenue depends on trading, a subtle misalignment appears. Even small shifts in behavior can affect outcomes.

Commission-based vs fiduciary models

Modern advisory firms increasingly follow fiduciary standards, meaning they must act in the client’s best interest.

Older models relied heavily on:

- Commission-driven sales models

- Product incentives

- Transaction-based revenue

That difference changes how advice is delivered.

Why this matters today

Even in 2026, investors still encounter legacy systems. Understanding these structures helps avoid confusion when evaluating firms with historical footprints like Craig Scott Capital, LLC.

Understanding Name Confusion Around “Newstown CraigScott Capital”

How confusion starts online

Search engines often combine old filings, news mentions, and unrelated content. This creates what experts call a digital footprint overlap.

As a result, online brand confusion becomes common, especially with financial firms that have changed structure over time.

Why identity confusion is risky

When investors cannot clearly separate:

- historical firms

- active companies

- archived data

they risk making decisions based on incomplete or outdated information.

Key principle

Name ≠ legal entity

That simple idea prevents most misunderstanding in financial research.

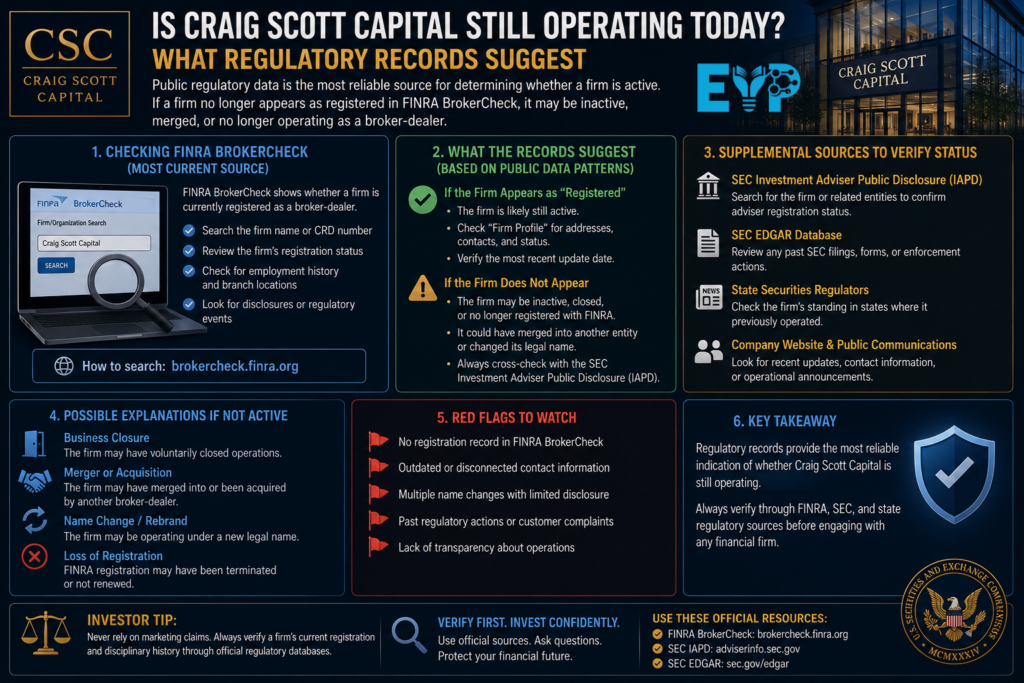

Is Craig Scott Capital Still Operating Today?

What regulatory records suggest

Public regulatory data is the most reliable source for determining whether a firm is active. If a firm no longer appears as registered in FINRA BrokerCheck, it may be inactive, merged, or no longer operating as a broker-dealer.

This is why verification matters more than search results.

What “inactive” really means

Inactive does not automatically mean illegal or fraudulent. It can also mean:

- Closure

- Acquisition

- Structural transition

However, it does mean the firm should not be treated as an active investment provider.

Key People and Leadership History

Why individuals matter more than brand names

In brokerage environments, individual brokers often carry more regulatory history than the firm itself. That’s why CRD records track both firms and professionals.

A firm’s reputation is often shaped by its registered representatives.

Why leadership history matters

Patterns in leadership can reveal:

- Sales culture

- Compliance priorities

- Risk tolerance

This is why regulators examine individuals alongside firms.

Investor Risk Analysis – What Went Wrong in Similar Firms

Misaligned incentives

When compensation depends on trading activity, investment risk increases for retail clients. This structure can lead to overtrading and reduced net returns.

Churning and excessive trading

Churning (excessive trading) is one of the most cited concerns in brokerage enforcement. Even small increases in turnover can reduce long-term performance due to fees and taxes.

Communication breakdowns

Another common issue is unclear communication around risk. Investors may not fully understand what they are buying, especially in complex products.

Practical Red Flags Investors Should Watch

Some warning signs appear repeatedly across problematic financial setups:

- Unclear registration or shifting identity

- Pressure-based sales conversations

- Complex products with unclear explanations

- Missing or inconsistent disclosures

These are not always proof of wrongdoing, but they signal information asymmetry.

How to Verify Any Brokerage Firm in 2026

Step 1: FINRA BrokerCheck

Start with FINRA BrokerCheck. It is the most reliable source for brokerage history and licensing.

Step 2: SEC verification

Check the SEC Investment Adviser Public Disclosure system for advisory registration and Form ADV filings.

Step 3: Match legal identity

Ensure the firm name matches its CRD number and legal records exactly.

Step 4: Review disclosures

Look for:

- Enforcement actions

- Customer complaints

- Terminations

Step 5: Confirm asset custody

Understand where your assets are held. Custody separation reduces risk significantly.

Financial Transparency vs Marketing Narratives

Marketing language often sounds polished. Words like “strategic wealth growth” or “advanced portfolio solutions” appear frequently online.

But real transparency shows up in:

- Regulatory filings

- Fee disclosures

- Custody clarity

In investing, regulatory proof beats marketing claims every time.

Modern Investment Firms vs Legacy Brokerages

Today’s platforms look very different from older brokerage models. Firms like Vanguard, Fidelity Investments, and Charles Schwab emphasize long-term investing, lower costs, and diversified portfolios.

Digital-first platforms like Betterment push robo-advisory and automated allocation strategies.

This shift reduces reliance on commissions and lowers conflict of interest.

Lessons Investors Can Learn

The biggest lesson from historical firms like Craig Scott Capital, LLC is simple.

Always understand:

- How your advisor gets paid

- Whether incentives align with your goals

- Whether trading activity actually benefits you

Long-term success usually comes from portfolio diversification, patience, and disciplined allocation rather than frequent trading.

Investor Due Diligence Checklist for 2026

Before trusting any financial firm, investors should:

- Verify registration status

- Check CRD numbers

- Review regulatory disclosures

- Compare advisory models

- Seek independent advice

This reduces exposure to investment fraud risks and improves decision quality.

Online Perception vs Regulatory Reality

Online discussions often mix outdated information with speculation. That creates information ambiguity, especially for legacy financial firms.

The safest approach is simple:

- Trust official regulatory databases

- Ignore unverified summaries

- Cross-check everything before investing

Investment Risks in Modern Retail Finance

Even in modern systems, risks remain:

- Market volatility

- Fee drag

- Liquidity risk

- Behavioral mistakes

Understanding these risks matters more than chasing returns.

What a Safe Investment Firm Looks Like Today

A trustworthy firm usually has:

- Clear fiduciary responsibility

- Transparent fee structure

- Strong regulatory compliance

- Independent asset custody

These factors reduce confusion and improve investor confidence.

How to Avoid Investment Scams

The safest approach is surprisingly simple:

- Slow down before investing

- Verify all registrations

- Ask direct questions about fees and risk

- Never rely only on online branding

Most scams rely on urgency and confusion. Removing urgency removes risk.

FAQs – Newstown CraigScott Capital (2026 Investor Guide)

1. What is Newstown CraigScott Capital?

Newstown CraigScott Capital / Craig Scott Capital, LLC is a name associated with a historical U.S. brokerage firm that appears in regulatory records. Investors often see it in archived or republished FINRA BrokerCheck data and online summaries, which can sometimes create confusion about its current status.

2. Is Craig Scott Capital still an active brokerage firm?

Public FINRA BrokerCheck records suggest that firms linked to CRD #155924 (Central Registration Depository number) may no longer operate as an active broker-dealer. However, exact status should always be confirmed directly through FINRA and SEC Investment Adviser Public Disclosure databases.

3. Why does “Newstown Craig Scott Capital” show up in search results?

This happens due to search engine visibility ≠ legitimacy issues. Old regulatory filings, archived pages, and content recycling often get indexed together. That creates online brand confusion, where historical and current data appear mixed.

4. What does FINRA BrokerCheck show about this firm?

FINRA BrokerCheck provides details like registration history, brokers involved, and any disclosure history or disciplinary records. For firms like Craig Scott Capital, LLC, it helps investors understand whether the firm was properly registered and how it operated under regulatory oversight.

5. What does SEC registration mean in this context?

SEC registration confirms whether a firm is authorized to operate as an investment adviser or related entity. Investors can verify this through SEC Investment Adviser Public Disclosure and Form ADV filings, which explain fees, structure, and potential conflicts of interest.

6. What risks are associated with firms like Craig Scott Capital?

Historical brokerage firms using commission-based revenue models often faced risks such as:

- Churning (excessive trading)

- Conflicts of interest in sales incentives

- High trading frequency impacting returns

- Reduced net investor performance due to fees and taxes

These risks are structural, not necessarily unique to one firm.

7. Does a regulatory record mean a firm is fraudulent?

Not necessarily. A disciplinary action or enforcement action can reflect compliance issues, reporting failures, or procedural violations. However, repeated or serious findings may indicate deeper regulatory compliance concerns that investors should take seriously.

8. How can I verify if a brokerage firm is legitimate?

You can verify any firm using:

- FINRA BrokerCheck for licensing and broker history

- SEC Investment Adviser Public Disclosure for advisory registration

- CRD number validation (e.g., CRD #155924)

- Legal entity name matching in official records

This is the core of proper brokerage firm verification.

9. Why do boutique brokerage firms often face scrutiny?

Many boutique brokerage firms operate under commission-driven sales models, which can create incentives for higher trading activity. This structure increases the risk of information asymmetry and conflicts between client outcomes and firm revenue.

10. What is the difference between brokerage firms and modern investment platforms?

Modern platforms like Vanguard, Fidelity Investments, Charles Schwab, and Betterment focus more on:

- Long-term investing

- Passive portfolio strategies

- Lower-cost advisory fees

- Reduced reliance on commissions

Older brokerage models often focused more on transaction-based revenue.

11. What is the biggest red flag investors should watch for?

One major red flag is confusion between brand identity and legal registration. If a firm cannot be clearly verified through FINRA BrokerCheck or SEC records, that is a sign to pause and investigate further before investing.

12. What should I learn from the Craig Scott Capital case?

The key lesson is that:

- Branding does not equal regulatory approval

- Online information can be outdated or mixed

- Proper investment due diligence checklist steps matter more than marketing claims

- Real safety comes from verified records, not search visibility

Final Investor Takeaway

The story behind Newstown CraigScott Capital is not just about one firm. It reflects how easily branding, history, and online visibility can blur together in financial research.

In investing, clarity always wins. Regulatory records, not search results, tell the real story.

Muhammad Bilal is an expert blogger specializing in meanings in text, delivering clear, engaging insights that help readers understand modern language, slang, and digital communication trends.